Stamp duty is a tax that all homeowners must pay when they purchase a house in the United Kingdom. The amount of the stamp duty tax differs according to the value of the property and whether you are a first time buyer or not. The rules are constantly changing and there are quite a few developments in regards to stamp duty in 2022. Let us take a look at what is new.

Two Massive Changes

Her Majesty’s Revenue and Customs are not quite happy with the current, seeming ‘advantages’ that mixed property buyers have received recently in regards to stamp duty. They believe mixed property buyers are being forced to pay a much higher sum.

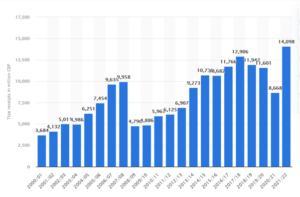

Stamp duty land tax receipts in the UK from 2000-2022 in million GBP

According to statistics, British homeowners paid approximately 14.1 billion pounds in stamp duty land tax for 2021-2022 in comparison to 8.4 billion pounds in 2020-2021.

What’s even more enraging is that the more expensive properties receive further deductions in the range of 7-12% for the mixed use of land on their property. Hence, two massive changes will be happening in regards to stamp duty in 2022. These changes are:

Apportionment

The most popular and widely accepted approach amongst the experts is apportionment, in which a mixed-use property’s reduced rate is applied exclusively to the portion of it that is non-residential land. This appears to be the most equitable answer to the ‘issue’ mentioned by HMRC, and it may also assist in clarifying the law in what has historically been a controversial area.

The threshold system

The other massive change we are talking about is the threshold system. In this case, a property may only be classified as mixed-use if it has a specified percentage of non-residential space.

This opens the door to considerably greater inequity for property buyers, as the physical percentage of a non-residential property does not often reflect the real nature of the property itself.

Imagine a block of apartments with a shop on the ground level, for example. While most of the property is residential, it falls under the mixed property category as shops are allowed to operate as well.

Streamlined Definition

The two changes mentioned above will give the homeowners some clarity by clear, streamlined definition between what is and is not residential property. This has been a major issue for quite some time. What’s worse, it has resulted in many tax-related cases in the court between homeowners and the HMRC arguing over the tax rates.

The possibility for controversy in these topics would be significantly reduced if HMRC factored in a clear definition by expanding the one that currently exists in the 2003 Finance Act. It would also make the jobs of tax experts and attorneys who work in real estate much easier.

SDLT Multiple Dwellings Relief Revision

HMRC believes that the Multiple Dwelling Relief (MDR) is causing misunderstandings since many homeowners are now making false claims. They state that from the entirety of the claims, around 40% are bogus while only 60% are actually legit.

The relief was designed to reduce the cost of SDLT in bulk residential property transactions in order to increase the availability of private rental accommodation. The relief is possible if two or more homes are purchased, even when a main house and a granny annex are purchased together.

However, the HMRC seeks ways to amend the current rules of the MDR. The relief basically functions by reducing the stamp duty rates for homeowners with multiple dwellings. However, the definitions of the MDR still remain doubtful as there is also a 3% surcharge for homeowners with multiple homes.

HMRC appears to be concentrating its efforts on MDR claims for houses with annexes or other structures on the property, such as cottages.

Conclusion

There have been many successful claims recently and HMRC is unhappy about it. Hence, they seek to amend the rules a bit. Some people might be upset with this decision. However, this helps in setting a clearer vision and path for stamp duty in the UK to tread on. Generally speaking, both advisors and taxpayers are happy about this.