What is multiple dwellings relief for SDLT?

Multiple Dwellings Relief (MDR) is a measure implemented by HMRC to encourage investment in residential property. It allows individuals or companies to claim relief on Stamp Duty Land Tax (SDLT) when purchasing multiple dwellings in a single transaction. This relief can be applied when buying multiple properties from a developer or when transferring properties from personal ownership to a limited company. MDR aims to reduce barriers and provide tax relief for those investing in residential properties. MDR can be claimed when purchasing more than one dwelling.

MDR, or Multiple Dwellings Relief, is a provision under Stamp Duty Land Tax (SDLT) that calculates the tax based on the average value of multiple properties being purchased, rather than the individual or total purchase prices. MDR applies to freehold or leasehold interests when purchasing multiple properties.

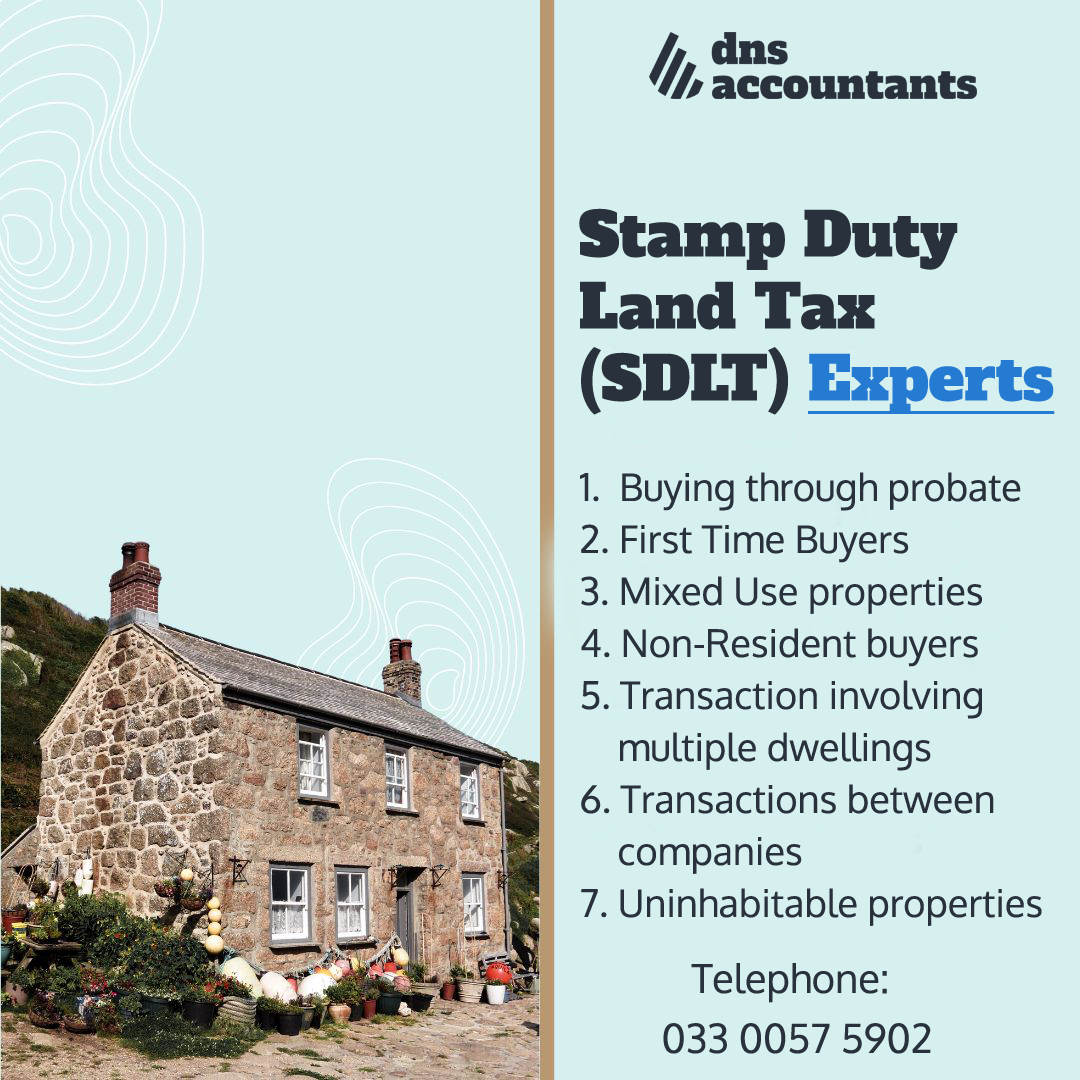

The relief for multiple residential rental properties can lower the rate of SDLT payable when specific conditions are fulfilled.

Consult Our Multiple Dwellings Relief (MDR) Experts

Multiple Dwellings Relief (MDR) Experts are professionals well-versed in the intricacies of the Multiple Dwellings Relief scheme, which offers potential savings to individuals and companies purchasing multiple residential properties in a single transaction.

These experts possess a deep understanding of the eligibility criteria, application process, and potential pitfalls associated with MDR.

With their specialised knowledge and experience, MDR Experts provide invaluable guidance to clients seeking to maximise the benefits of this relief while ensuring compliance with all relevant regulations and requirements. Trusted advisors in the field of property taxation, MDR Experts play a crucial role in helping clients navigate the complexities of multiple dwelling transactions with confidence and efficiency.

To discuss your position, please contact our SDLT experts and book a telephone or face to face consultation.

5 based on 800 reviews

5 based on 800 reviews